Training Centre

Get the training you need, when you need it.

Get the training you need, when you need it.

Learn how to apply and lodge applications using Granite’s broker digital loan application platform, powered by Simpology V2 with Loanapp 2.0.

Explore step-by-step training guides for the Granite Simpology Loanapp V2 experience.

How to set up an SMSF application in Loanapp V2

A Self-Managed Super Fund (SMSF) loan allows an SMSF to borrow funds to purchase an investment property through a Limited Recourse Borrowing Arrangement (LRBA).

Under an LRBA, the lender’s recourse is generally limited to the property held within the borrowing arrangement and does not extend to the SMSF’s other assets in the event of default.

Due to the legal structure required under superannuation legislation, SMSF applications involve multiple entities and a more complex applicant structure than a standard residential mortgage application. Correctly configuring these entities in Loanapp V2 is critical to ensure accurate lender assessment and successful application submission.

A typical SMSF application in Loanapp V2 consists of the following entities:

| Applicant | Entity Type | Role in Application |

| Pty Ltd Company (SMSF Trustee) | Company | Primary Borrower |

| SMSF Trust | Trust | Co-Borrower |

| Pty Ltd Company (Bare Trustee) | Company | Guarantor + Security Holder |

| Bare/Security/Custodian Trust | Trust | Guarantor |

| Individual Members (e.g. Mr & Mrs Smith) | Person | Guarantor/s |

Follow each step in order. Do not skip ahead — the applicant structure must be complete before entering financial details.

| Step | Action | Key Requirement |

| 1 | Enable SMSF Toggle | In the Setup screen, toggle SMSF to YES before anything else |

| 2 | Add SMSF Trustee (Pty Ltd) | Set as Primary Borrower |

| 3 | Add SMSF Trust | Set as Co-Borrower |

| 4 | Add Bare Trustee (Pty Ltd) | Set as Guarantor |

| 5 | Add Bare Trust | Set as Guarantor |

| 6 | Add Individual Person(s) | Individual SMSF members — set as Guarantors |

| 7 | Complete Entity Details | Fill in all Company/Trust detail screens; link trustees to entities |

| 8 | Complete Personal Details | Person Applicant and super contributions (not required for Easy Refi) |

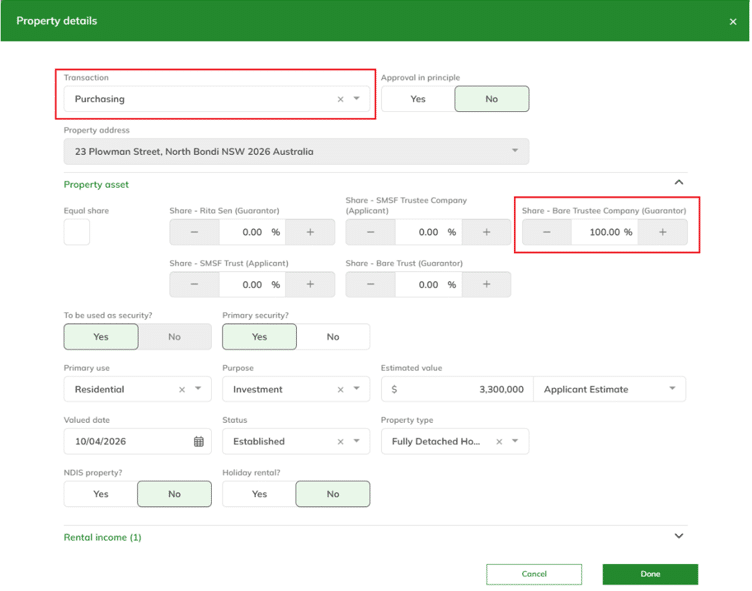

| 9 | Add Security Property | Ownership must be 100% to the Bare Trust Company |

| 10 | Confirm Loan Details | Verify Primary Borrower (Pty Ltd) is listed as the Borrower |

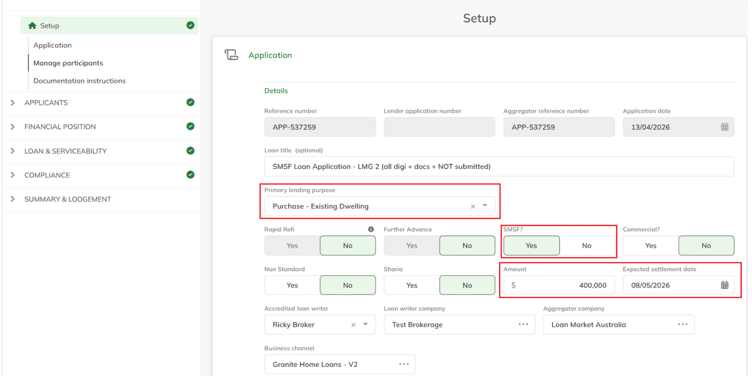

When creating a new application, you will first be presented with the Setup screen. This is where the high-level application details are configured, including the application title, loan amount, and anticipated settlement date.

⚠ Important: Toggle the SMSF question to YES before adding any applicants. This activates SMSF-specific fields and logic throughout the application.

📷 Screenshot: Setup screen — SMSF toggle set to YES (Click image to enlarge)

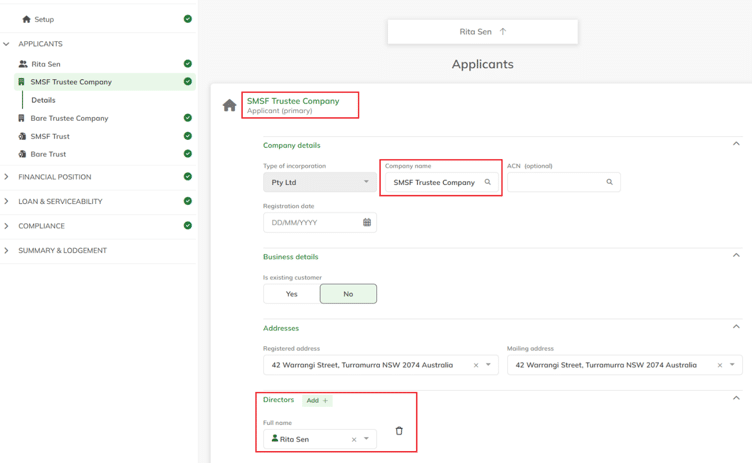

The Primary Borrower is the Pty Ltd company that acts as Trustee for the SMSF.

✓ Tip: You can use the company ABN Lookup feature – if this is the correct company, the lookup result will show it as an ATO Regulated SMSF — a useful confirmation you have the right entity.

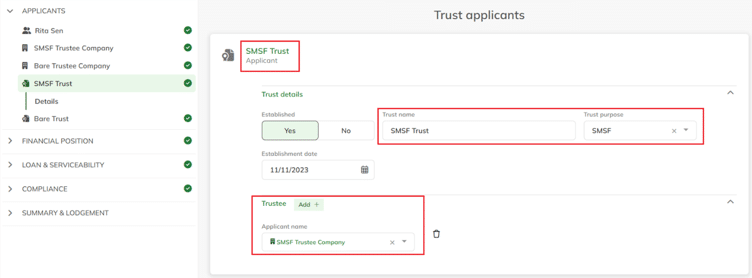

The next applicant to be added is the SMSF Trust, which represents the superannuation fund itself.

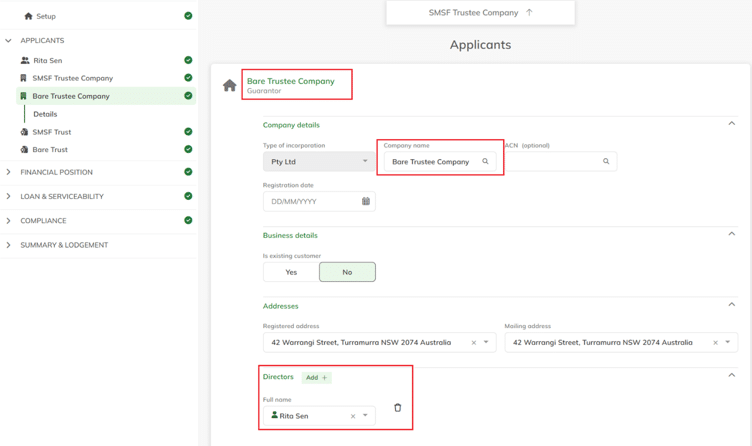

The next applicant to be added is the Bare Trust Pty Ltd Company, which acts as the trustee of the Bare (Security/Custodian) Trust. This entity is responsible for legally holding the security property on behalf of the SMSF structure during the loan term.

⚠ Security Property Ownership: This Bare Trust Pty Ltd company is the entity that will be set as the 100% owner of the security property in Step 9.

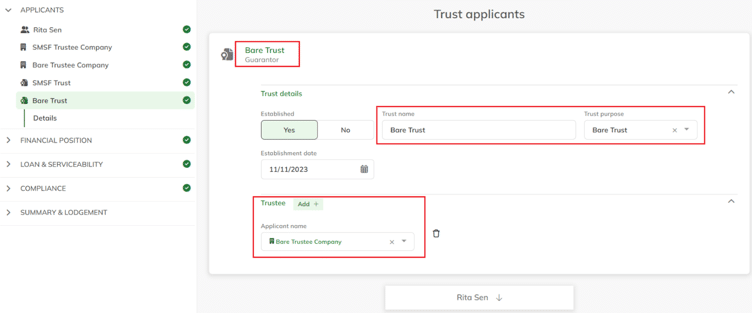

The Bare Trust (also referred to as the Security Trust or Custodian Trust) holds legal title to the property on behalf of the SMSF until the loan is fully repaid.

The individual members of the SMSF are added as personal guarantors for the loan. Depending on the SMSF structure, there may be one or multiple member guarantors.

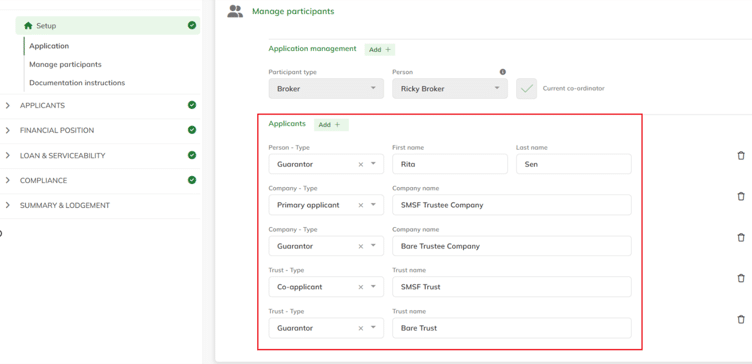

Once all applicants have been added, your application structure screen should show all five parties listed. You are now ready to complete the detail for each entity.

📷 Screenshot: Full applicant structure — all applicants listed (Click image to enlarge)

You must complete the detail screens for each of the four entity applicants. Navigate to each entity in turn:

Primary Borrower Company (SMSF Trustee)

📷 Screenshot: Primary Borrower company details screen with Directors/Shareholders

(Click image to enlarge)

SMSF Trust

📷 Screenshot: SMSF Trust details screen — Trustee linked to Company, Beneficiaries listed (Click image to enlarge)

Bare Trustee (Guarantor)

📷 Screenshot: Bare Trust Company details screen with Directors/Shareholders

(Click image to enlarge)

Bare/Security/Custodian Trust (Guarantor)

📷 Screenshot: Bare Trust details screen — Trustee linked to Bare Trust Company

(Click image to enlarge)

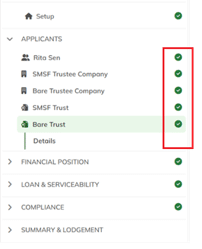

✓ Completion Check

When all entity detail screens are complete, the Applicants panel will display a green tick against each applicant. If any applicant still shows a warning icon, click into their screen to identify and complete the missing fields.

📷 Screenshot: All applicants with green completion ticks (Click image to enlarge)

Navigate to the Financial Position page for each applicant. The level of detail required varies by entity type:

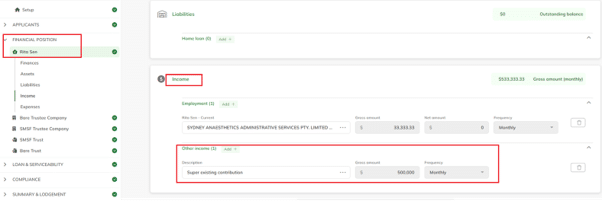

Super Contributions (not required for Easy Refi)

For each Person Guarantor, you must enter the superannuation contributions being made to the SMSF (if applicable). This is entered in the Income section under Other Income:

📷 Screenshot: Income screen — Other Income section for super contributions

(Click image to enlarge)

When entering the security property, ownership must be assigned to the Bare Trust Company — not the SMSF Trust or the individual guarantors.

📷 Screenshot: Security property screen — ownership set to Bare Trust Company at 100%

(Click image to enlarge)

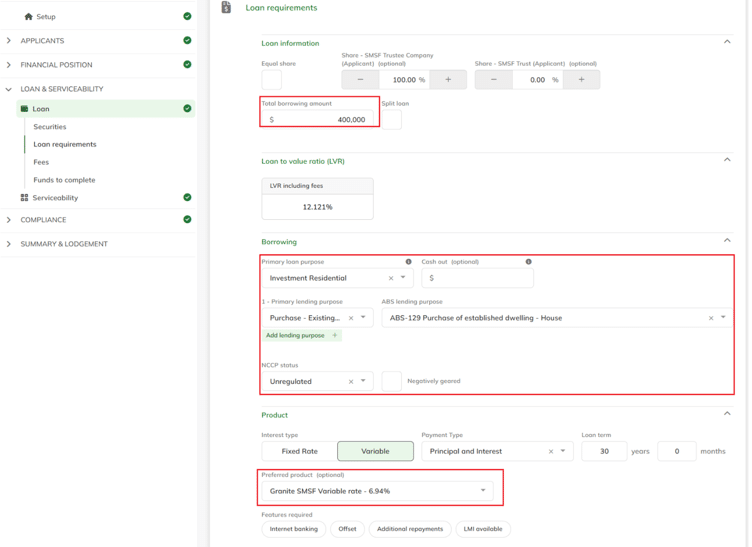

In the Loan Details section, confirm that the Primary Borrower (SMSF Trustee) is recorded as the Borrower for the application.

📷 Screenshot: Loan Details screen — Primary Borrower Pty Ltd confirmed as Borrower

(Click image to enlarge)

Entering SMSF Applications in Loanapp V1

An overview of SMSF structure (for LRBA and structure for LoanApp), step by step guide on how to enter into the system.

Conducted by Danielle from our Broker Support Team.

Need more info? Click here to find your Partnership Manager or Broker Support contacts.

How To respond to Lender’s Missing Information Requests (MIRs) in Loanapp V1

An overview of respond to missing information request via Simpology.

Conducted by Don from our Broker Support Team.

Need more info? Click here to find your Partnership Manager or Broker Support contacts.

Uploading Supporting Docs into Loanapp V1

An overview of how to upload supporting documents into Simpology.

Conducted by Don from our Broker Support Team.

Need more info? Click here to find your Partnership Manager or Broker Support contacts.

Key product policies

Professional Self Employed are consumers who are, but are not limited to,

The table below details acceptable employment history.

| Type | Requirements |

|---|---|

| Permanent full time |

|

| Permanent Part Time |

|

| Casual |

|

| Contract |

|

| Second Job |

|

| Self Employed |

|

The table below details the acceptable and unacceptable types of Australian Income:

| Type | Requirements |

|---|---|

| Salary and Wage |

|

| Overtime and Allowances |

Eligible Occupations1

All Other Occupations

|

| Bonuses and Commissions |

|

| Salary Sacrifice |

|

| Salary Packaging |

|

| Novated Lease |

|

| Car Allowance |

|

| Fully maintained company car |

|

| Self Employed |

|

| Company Income |

|

| Trust Distribution |

|

| Rental Income |

|

| Investment Income |

|

| Australian Government Bond Income |

|

| Family Tax Benefit (as supporting income only) |

|

| Child Maintenance (as supporting income only) |

|

| Employer Maternity Leave Payment / Paid Parental Leave Payment |

|

| Social Security Benefits & Government Pensions |

|

| Income Protection & TPD Income |

|

| Unemployment & Sickness Benefits |

|

| Worker’s Compensation |

|

| Income from Boarders |

|

1 Ambulance Officer, Police, Firefighter, Nurse, Midwife, Paramedic, Border Force, Protective Services Officer, Medical Practitioner Training, Anaesthetist, Dermatologist, Emergency Medical Specialist, Obstetrician, Gynaecologist, Ophthalmologist, Paediatrician, Pathologist, Specialist Physician, Psychiatrist, Radiologist, Nurse Educator, Nurse Researcher, Dentist, Dental Specialist, Hospital Pharmacist, Industrial Pharmacist, Retail Pharmacist, Occupational Therapist, Optometrist, Physiotherapist, Speech Pathologist, Chiropractor, Osteopath, Podiatrist, Medical Diagnostic Radiograph, Radiation Therapist, Nuclear Medicine Technologist, Sonographer, Veterinarian, Dietitian, Naturopath, Acupuncturist, Natural Therapy Professionals, Audiologist, Orthoptist, Orthodontist.

The table details the acceptable types of foreign income:

| Type | Requirements |

|---|---|

| Salary or Wage |

|

| Overtime |

|

| Allowances |

|

| Bonus / Commissions |

|

| Self Employed |

|

| Rental Income |

|

| Investment Income |

|

Standard Commercial Properties are properties that are used for business purposes. This includes owner occupier, leased from related entity and tenanted properties.

The acceptable commercial property security types include:

Standard Commercial Properties are properties that are used for business purposes. This includes owner occupier, leased from related entity and tenanted properties.

The acceptable commercial property security types include:

Access these policy changes, which came into effect on the 9 March 2026

Access these policy changes, which came into effect on the 18 May 2026

Easy Refi SMSF Loan Servicing calculator

How to use the Granite Easy Refi SMSF Loan Servicing calculator

SMSF Loan Servicing calculator

How to use the Granite SMSF Loan Servicing calculator for purchases

We have compiled a comprehensive guide on investing in NDIS housing, focusing specifically on Specialist Disability Accommodation (SDA). This guide outlines the key factors to consider when investing in SDA properties. It aims to help investors make informed decisions while contributing to the availability of high-quality and accessible housing for individuals with disabilities.

(Note: Home loans for SDA properties are not currently available through Granite.)

Download NDIS Information Guide© 2026 Granite Home Loans Pty Ltd

Digital consent

Digital consent Digital credit checks

Digital credit checks Digital ID verification

Digital ID verification Digital valuations

Digital valuations Docusign

Docusign